Precision Mining

Jun 2026 | 15 Minutes

Jun 2026 | 15 Minutes

The global precision mining technology landscape is undergoing a profound transformation driven by scientific breakthroughs, strategic national investments, and accelerating commercial readiness. While energy transition, EV adoption, and semiconductor supply chain pressures continue to push global demand for critical minerals, miners face mounting pressure to cut costs, meet tighter environmental standards, and accelerate production. Precision Mining has emerged as the technological response to these pressures by integrating AI, autonomous systems, advanced sensing, and real-time analytics to optimize every stage of the mine lifecycle, from exploration through to processing and remediation. Governments across North America, Europe, and Asia have moved from policy statements to binding investment commitments, compressing project timelines and creating direct commercial pull for technologies that improve ore recovery, reduce costs, and accelerate permitting. The total addressable market for precision mining technology is conservatively in the USD 35 to 52 billion range by 2034, growing at double-digit rates. However, patent filings heavily skewed by China in the sector reveal a significant IP gap for Canadian and Western companies.

IAC’s Precision Mining IP Intelligence Report examines this evolving ecosystem through the lens of intellectual property, offering a deep dive into the competitive landscape and innovation trends across Exploration & Surveying, Material Extraction & Handling, Mining Techniques, Data Analytics & Software, Mineral Processing & Beneficiation, and Sustainability & Environmental Solutions. The report also maps the Precision Mining value chain across seven segments: Exploration & Surveying, Material Extraction, Drilling & Blasting, Processing, Smelting, Waste Management, and Software to reveal competitive positioning and partnership or investment opportunities. By integrating patent intelligence with market research, this study provides a clear view of the current precision mining landscape and its likely direction of travel. It is intended to equip industry stakeholders, investors, and policymakers with actionable, evidence-based insights to inform strategic decision-making across the Precision Mining sector.

7,563 patent families (9,070 patent publications) were analyzed for this report. These patents were categorized into various technologies using a technology taxonomy as seen below.

Geospatial Analysis (1,473)

• Remote Sensing & Imaging

• Mapping & GIS Technologies

• Photogrammetry

• Light Detection and Ranging (LiDAR)

Geophysical Analysis (387)

• Magnetic Surveys

• Seismic Reflection & Refraction

• Ground Penetrating Radar (GPR)

• Gravity Surveys

• Induced Polarization (IP)

Geochemical Analysis (175)

• Soil Sampling & Analysis

• Stream Sediment Sampling

• Rock Chip Sampling

• Biogeochemical Surveys

Environmental Monitoring (782)

• Autonomous Haulage Systems (AHS) (796)

• Conveyor Systems & Technologies (155)

• Fleet Management Systems (492)

• Automation & Robotics (2,386)

• Ore Sorting & Grade Control (535)

• Automated Maintenance Systems (687)

Drilling Technologies (795)

• Drilling Methods

• Drilling Equipment

• Precision Drilling Techniques

Blasting Technologies (450)

• Blasting Techniques

• Explosive & Detonation Methods

• Blasting Management Systems

Autonomous Drilling/ Blasting Systems (451)

• Predictive Maintenance Software (269)

• AI and Machine Learning for Mining Operations (2,059)

• Digital Twin Technology (687)

• IoT & Sensor Integration (5,051)

• Mine Planning Simulations (593)

• Drilling/Blasting Simulations (580)

• Separation Technologies (52)

• Concentration Techniques (15)

• Dewatering and Drying (79)

• Agglomeration Methods (5)

Waste Management (174)

• Tailings Management Systems

• Zero-waste Mining Technologies

Water Management (251)

• Water Recycling

• Water Treatment

Emission Control (1,052)

• Carbon Capture in Mining

• Dust Suppression Systems

• Eco-friendly Blasting Techniques

Fig. 1.1 Technology Taxonomy for Precision Mining

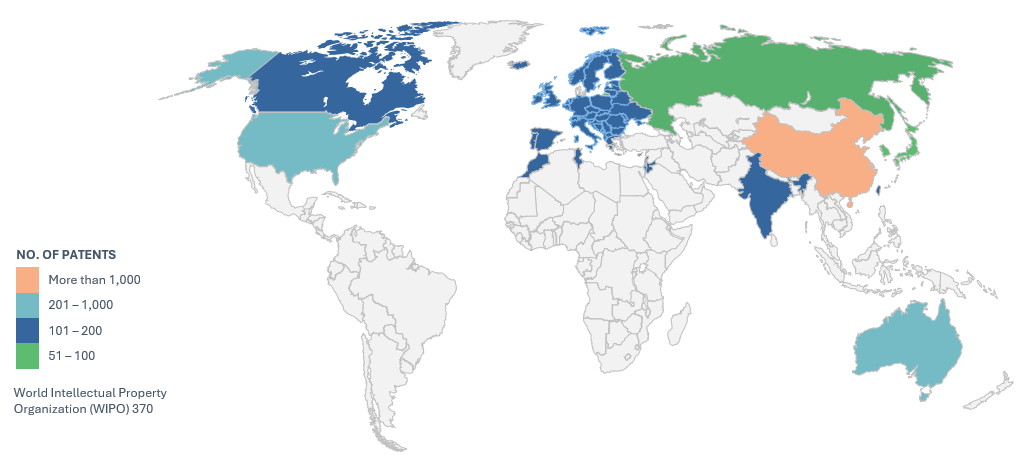

Patent activity in Precision Mining is heavily concentrated in China, mirroring trends seen across other technology-intensive sectors. Chinese entities, primarily universities, state-owned enterprises, and large mining conglomerates account for the dominant share of filings across all six technology domains. Chinese institutions such as China University of Mining and Technology, CCTEG and Shandong University of Science & Technology are particularly prolific, with deep portfolios in automation, data analytics, and autonomous haulage systems. These filings accounted for ~91% of total filings. By comparison, there were 341 patent filings in the U.S., 232 in Australia, 370 at WIPO (through the Patent Cooperation Treaty, PCT), and 120 in India. Only 115 patent applications were filed in Canada within the scope of the study. Overall, China’s dominant contribution to patent filings in precision mining highlights the strategic importance of IP protection for Canadian and Western companies protecting innovations in global markets.

Canada: 115

Granted: 32 (27.8%)

Apps: 76 (66.1%)

USA: 341

Granted: 208 (61%)

Apps: 87 (25.5%)

EP: 117

Granted: 49 (41.9%)

Apps: 51 (43.6%)

India: 120

Granted: 18 (15.0%)

Apps: 98 (81.7%)

Russia: 69

Granted: 48 (69.6%)

Apps: 6 (8.7%)

China: 7,169

Granted: 2,003 (27.9%)

Applications: 2,395 (33.4%)

Utility Models: 1,723 (24.0%)

Japan: 98

Granted:56 (57.1%)

Apps: 25 (25.5%)

Utility Models: 1 (1.0%)

Republic of Korea: 63

Granted: 46 (73.0%)

Apps: 12 (19.0%)

Australia: 232

Granted: 101 (43.5%)

Apps: 90 (38.8%)

Notes: The chart reflects the number of patent publications (not patent families) attributed to each country shown. European Patent Office (EPO) data includes filings from all member states of the European Patent Organization. Total patent records comprise granted patents, active pending applications, and utility patents; expired and other inactive filings account for the remaining difference.

Fig. 1.2 Geographic distribution of patent filings in Precision Mining

Data Analytics & Software is the dominant technology domain by a wide margin, accounting for 6,019 patent families (79.6% of total), peaking at 1,363 filings in 2024 and reflecting the industry’s shift toward AI/ML, digital twins, and IoT-driven mine intelligence. More specifically, IoT & Sensor Integration leads at 5,051 families (67%), followed by Automation & Robotics at 2,386, AI & Machine Learning at 2,059, and Geospatial Analysis at 1,473.

Exploration & Surveying accounts for 2,204 patent families (29.1%), covering geospatial analysis, remote sensing, and subsurface modelling. Mining Techniques (1,444 families) covers Drilling Technologies, Blasting Techniques, and Autonomous Drilling/Blasting Systems. Sustainability & Environmental Solutions reached 1,373 families (18.2%), hitting a new record of 281 filings in 2024, reflecting growing pressure on ESG compliance. IAC’s full report dives deeper into technology analysis while highlighting key assignees by jurisdiction, and the IP whitespace opportunities available to Canadian companies in under-patented niches.

Chinese academic and state-backed institutions hold the dominant share of patent ownership in precision mining technologies. A smaller share of filings is spread across mining companies, and equipment OEMs. China University of Mining & Technology leads globally with 513 patent families, followed by CCTEG (324), Shandong University of Science & Technology (157), and Xi’an University of Science & Technology (139). Outside China, global leaders among Western OEMs include Caterpillar (12 families ex-China), Sandvik Mining (9), and Epiroc (9), primarily focused on autonomous haulage, IoT integration, and drilling automation.

Canada holds world-class mineral endowment and the most comprehensive critical minerals policy stack of any jurisdiction, yet its patent presence in Precision Mining is strikingly thin. Patent filings at CIPO totaled only 115 patent publications across the study period: 32 granted and 76 pending which is a fraction of global output that bears no relation to the sector’s economic weight.

However, Canadian companies hold only 13 patent families filed domestically. The gap between operational expertise and patent footprint represents the most critical and the most addressable risks for Canadian precision mining companies seeking global scale. Without strong IP portfolios, companies miss out on licensing revenues and face challenges in negotiating partnerships with major OEMs, often falling behind competitors with more robust patent holdings.

The full report details filing trends by technology, Canadian and foreign assignee breakdowns, global protection coverage of Canadian companies, and specific IP strategy recommendations.

Note: The charts above are based on patent families

Fig. 1.3 Top filers in Canada – Precision Mining

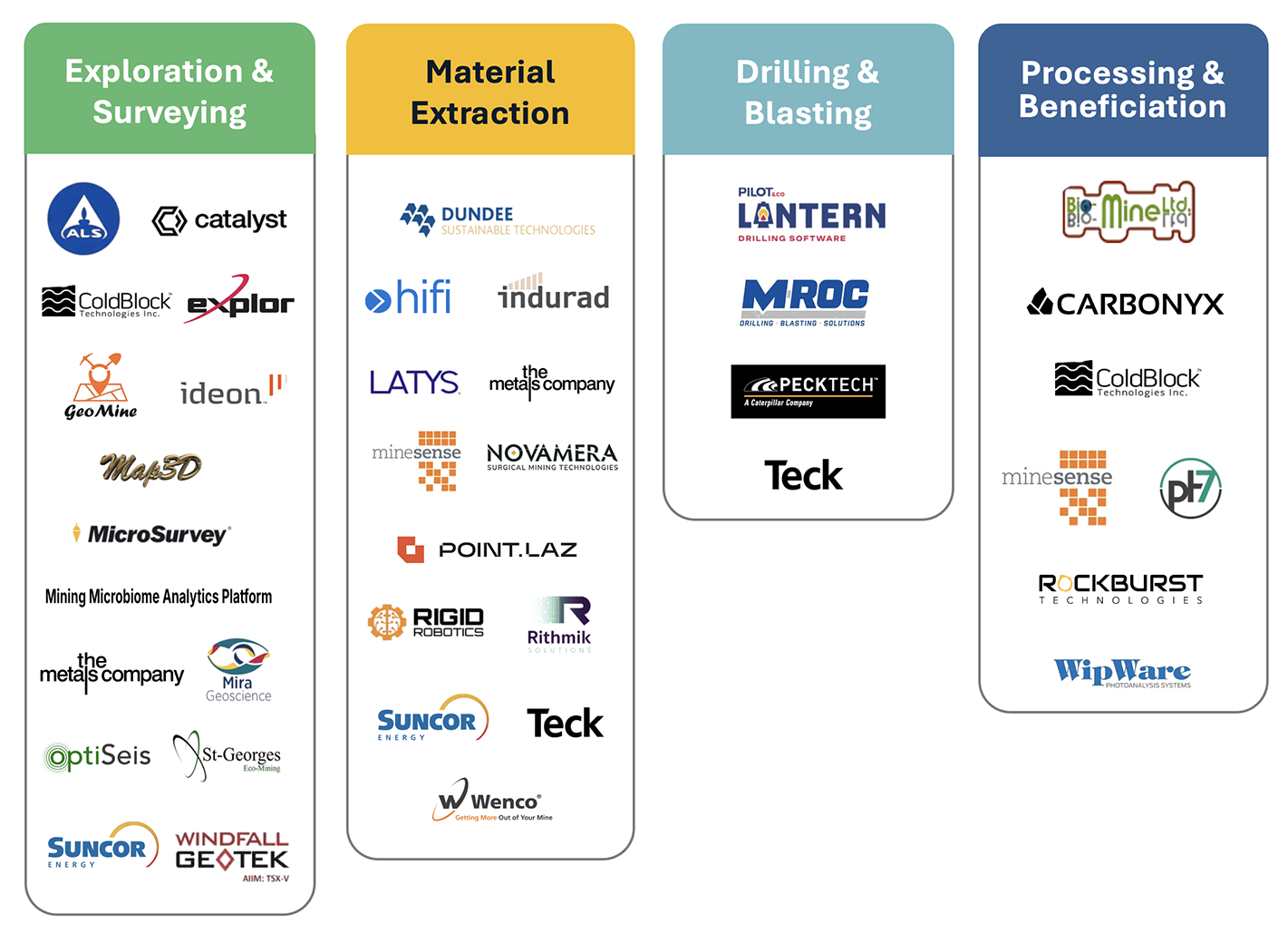

The categories shown in Fig. 1.4 represent the sector value chain. The Canadian companies operating in the value chain is depicted below. Access the full report for the global value chain.

Fig. 1.4 Canadian value chain – Key players in Exploration & Surveying and Material Extraction segments of Precision Mining

SMEs face structural risks as the precision mining landscape consolidates rapidly, with OEMs like Caterpillar, Sandvik, Epiroc and Komatsu building closed sensing-to-decision ecosystems through acquisition. China holds approximately 91% of global precision mining patent families, weakening Freedom to Operate for any company entering new global markets. Independent technology companies risk platform lock-out unless they demonstrate clear interoperability or occupy a niche the OEM has not yet absorbed.

Patent Portfolio Development – Strive to build a robust patent portfolio that protects your innovations and deters competitors. Without a significant portfolio of patents, a smaller company involved in an IP dispute with a large company typically lacks the leverage that the ability to counter assert provides. The primary purpose of IAC’s Portfolio is to provide patents that can be counter asserted against companies with large portfolios that could pose a risk to member companies. Read more about IAC’s Patent Portfolio here.

Geographical Considerations – Assess patent rights on a country-by-country basis, as patent laws and enforcement practices vary across jurisdictions. A product or service that may be covered by a patent in one country may not be in another because a similar patent may not exist or be active elsewhere, and the claims may have different scopes.

IP Strategy & Ownership: Prioritize the protection of your intellectual property and put in place strategies to increase its value. These steps are a good start towards increasing your Freedom-To-Operate. IAC’s IP Upskilling program empowers companies to develop and maintain solid, scalable, forward-thinking IP and data strategies.

For a comprehensive overview of these and additional IP strategies, including detailed patent and market data on key players, trends, and jurisdictional considerations, refer to the full report.

Submit the form below to download the report.

Disclaimer: The content of this document may have been derived from information from third-party databases, the accuracy of which cannot be guaranteed. IAC hereby disclaims all warranties, expressed or implied, including warranties of accuracy, completeness, correctness, adequacy, merchantability and/or fitness of this document. Nothing in this document shall constitute technical, financial, professional, or legal advice or any other type of advice, or be relied upon as such. Under no circumstances shall IAC be liable for any direct, indirect, incidental, special, or consequential damages that result from use of or the inability to use this document.

See how our IP expertise can support your business.